Nigeria has one of the most challenging inflation environments in Africa. In the last three (3) years, inflation has eroded the wealth of many who believed their money was growing because the balance in the bank account were increasing, when in reality, inflation has consistently outpaced savings rates, reducing the real value of money over time.

Understanding the effect on purchasing power is one of the most important lessons an investor can learn.

| 2025 (₦) | 2026 (₦) | Rate of Change | |

|---|---|---|---|

| Savings Balance | 500,000.00 | 535,000.00 | 7.00% (Avg. Savings rate) |

| Cost of Goods & Services | 500,000.00 | 578,450.00 | 15.69% (Inflation rate) |

| Real Return | -43,450.00 | -8.69% |

[Caption] *Source: Central Bank of Nigeria (CBN)

If you placed ₦500,000 in a savings account. One (1) year later, your account balance increased to ₦535,000, representing a 7% return. It appears you made a good investment.

Factoring inflation at 15.69% for the same period, the prices of goods and services in the inflation basket rose significantly faster than savings rate. What ₦500,000 could buy the previous year would now cost ₦578,450.

This means that despite the increase in your account balance, your money actually lost purchasing power in real terms. In other words, your savings grew nominally, but became weaker because inflation outpaced your return.

In real terms, your money lost approximately ₦43,450 in purchasing power, even though your account balance increased.

This difference between nominal returns and real returns is the hidden danger of inflation. A growing bank balance does not always mean growing wealth. The true measure of wealth is not how much money you have, but what that money can actually buy.

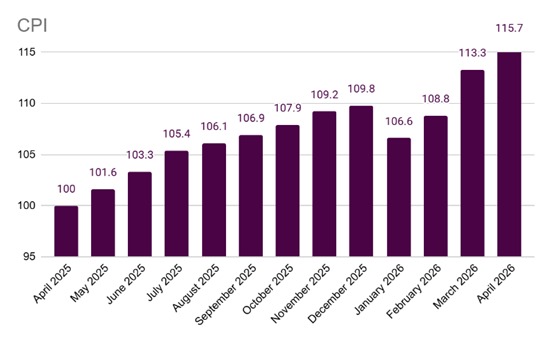

[Caption] Consumer Price Index (CPI) in Nigeria (Change in price of goods and services) starting in 100

What Inflation Is?

Inflation is the sustained rise in the general price level over time. When things cost more today than last year, your naira has lost value, even if your account balance has not changed.

In Nigeria, inflation is measured by the Consumer Price Index (CPI), published monthly by the National Bureau of Statistics (NBS). The NBS tracks the cost of a broad basket of goods and services and measures how it changes over time. The two most watched components are food inflation and core inflation, which strips out food and energy to reveal underlying price trends.

The Number That Actually Matters, Real Return

The distinction between nominal return and real return is one of the most important concepts in investing.

Your nominal return is the interest rate on your savings account, the coupon on a bond, the yield on a fund.

Your real return is what you actually gain after inflation eats into it:

Real Return ≈ Nominal Return − Inflation Rate

Your Main Options as a Nigerian Retail Investor

Money Market Funds pool capital into short-term instruments and offer daily liquidity at yields that track the interbank market rate. For most Nigerian retail investors starting out, they are the most practical way to earn returns that at least keep pace with inflation.

Treasury Bills. They are short-term instruments (91, 182, or 364 days) issued by the CBN on behalf of the Federal Government. They are among the safest investments available. The risk is that yields follow the CBN’s policy rate. When rates fall, T-Bill yields can compress below inflation.

FGN Savings Bonds are issued monthly by the Debt Management Office with two- and three-year tenors and quarterly coupon payments. They are low-risk and designed for retail investors. The trade-off is illiquidity. Your money is locked in, and if inflation rises above your coupon rate, your real return turns negative.

Dollar-Denominated Assets such as Eurobonds, dollar savings accounts, and US market exposure have served as a purchasing power hedge during periods of severe naira depreciation. They carry their own risks, but a portion of savings in dollars has historically protected Nigerian investors from naira-specific erosion.

NGX Equities represent ownership in companies. Over the long run, stocks have historically delivered the strongest real returns of any asset class because companies can raise prices and grow earnings alongside a growing economy.